Stocks Rise Early as U.S. and Iran Pause Attacks

Published as of: July 27, 2026, 9:10 a.m. ET

Listen to this update

Listen here or subscribe to the Schwab Market Update in your favorite podcast app.

| The markets | Last price | Change | % change |

|---|---|---|---|

| S&P 500® Index | 7,411.98 | +3.68 | +0.05% |

| Dow Jones Industrial Average® | 51,947.25 | +235.60 | +0.46% |

| Nasdaq Composite® | 24,975.82 | -161.87 | -0.64% |

| 10-year Treasury yield | 4.65% | +0.03 | -- |

| U.S. Dollar Index | 101.38 | -0.09 | -0.08% |

| Cboe Volatility Index® | 17.72 | -0.86 | -4.63% |

| WTI Crude Oil | $84.21 | -$5.10 | -5.71% |

| Bitcoin | $65,055 | +$840 | +1.31% |

(Monday market open) Stocks jumped higher early and oil prices dove more than 5% after President Trump decided against a major escalation in Iran and both sides paused military attacks. Treasury yields fell as concerns about inflation and interest rates eased.

Today is relatively quiet on the earnings and economic front, though June's durable goods orders kicked things off, coming in at a gain of 0.4%, well below the consensus estimate of 2%. Earnings ramp up tomorrow and for the remainder of the week, with four of the Magnificent 7—Microsoft (MSFT), Meta (META), Apple (AAPL), and Amazon (AMZN)—visiting the earnings confessional on Wednesday and Thursday. The Federal Reserve rate decision comes Wednesday.

Market averages were mixed on Friday, initially rebounding amid cautious hopes for renewed peace talks between the U.S. and Iran that sent oil prices lower. Stocks began to lose steam as the close approached, however, following President Trump's Friday afternoon promise to levy "substantial" additional tariffs on the EU—claiming unfair treatment of U.S. tech companies—and continued threats of additional military action. Chip stocks were pummeled again, but 10 of 11 S&P 500 sectors closed in positive territory. For the week, the Dow and S&P 500 moved modestly lower while the Nasdaq Composite, weighed down by continued profit-taking in the chip sector, gave back 2.13%.

To get the Schwab Market Update in your inbox every morning, subscribe on Schwab.com.

Three things to watch

- Odds of a rate hike rise: The odds narrowly point to a relatively ordinary Fed meeting this week, as the CME FedWatch Tool shows a 64% chance of rates being held on Wednesday. Chances of a hike are now at 36%, up from about 13% on June 17. Brent crude's recent move back near the $100-per-barrel area is largely behind this shift, said Collin Martin, head of fixed income research and strategy at the Schwab Center for Financial Research (SCFR). "The cool June CPI print was a step in the right direction, but higher energy prices mean that we should see that reversed in the July readings," he added. It's possible, though, that the central bank will wait to see more evidence of "hot" inflation data before pulling the rate-hike trigger. The last time the central bank hiked rates was in July 2023; rates have been steady since a 25-basis-point cut in December 2025.

- Bears coming out of the woodwork: Last week, bullish sentiment as measured by the American Association of Individual Investors (AAII) dropped 15 percentage points to 29.6%, well below the historical average of 37.5%. Bearish sentiment, meanwhile, jumped almost 10 percentage points to above 42% from 32.9% the week prior. This put the bull-bear spread at an unusually low -12.8%, versus the historical average of 6.5%. The AAII's question of the week concerned inflation: 41.1% of respondents said they expected second-half inflation to be on par with the first half of the year. Meanwhile, 31.4% said they believed it would be higher, while 23.2% expected inflationary pressures to slow.

- New home sales send mixed messages: June new home sales rose 1.6% month over month to 628,000, topping analysts' expectations of 620,000 but sagging 5.6% year over year. May sales numbers were revised higher to 618,000 from 580,000. The affordability question remains key but seems to be improving slightly. While the average selling price is just under half a million, at $475,400, this is down 9.5% from May 2026 and 6.5% below the average June 2025 price. The West was the most expensive region and (perhaps not coincidentally) saw the only drop in month-over-month sales—a notable retreat of 22.4%. Mortgage rates hovered near 6.5% in June, per Freddie Mac. Heading into the final week of July, this reading has inched higher still, to 6.58%—the highest weekly average in almost a year. May's S&P Cotality Case-Shiller Home Price Index is due tomorrow at 9 a.m. ET, with analysts expecting 1.1% year-over-year jump in home prices.

On the move

- Alphabet (GOOGL) rebounded slightly on Friday after a sharp earnings-related plunge the previous session. For the week, the tech giant shed almost 9%. It gained more than 1% in early trading Monday.

- Apple (AAPL), which has been relatively restrained in AI-related capital spending, stood out among the Magnificent Seven Friday, gaining about 3.5% amid jitters over the scale of capital spending by some of its peers.

- Semiconductor companies gained some ground in pre-market trading after getting hit the hardest Friday. Sandisk (SNDK) fell 11% Friday, and Intel (INTC) and ARM Holdings (ARM) both lost about 8%, while Marvell (MRVL) and Micron (MU) both dropped about 7%.

- Broadcom (AVGO) rose about 2% before the bell after Samsung Electronics announced over the weekend that the two companies would deepen their partnership in the chips space.

- Data storage companies Seagate Technology (STX) and Western Digital (WDC) both lost about 7% Friday. Both were up more than 2% in early trading.

- AI cloud providers were hammered again Friday amid broad concerns about capital spending. Nebius Group (NBIS) tumbled 15%, while CoreWeave (CRWV) lost more than 11%, and IREN (IREN) lost more than 8%.

- Verizon (VZ) gained nearly 6% Friday after reporting earnings that topped estimates and announcing it had signed a deal to provide dark fiber connectivity for Google's data centers.

- Energy stocks fell alongside oil prices in early trading. Chevron (CVX) and ExxonMobil (XOM) both lost nearly 3%. Devon Energy (DVN) lost nearly 4%.

- Energy technology company Baker Hughes (BKR) gained more than 2% in pre-market trading after reporting earnings and revenue that topped estimates.

- Delta Air Lines (DAL) gained nearly 3% and United Airlines (UAL) jumped nearly 4% before the bell on the prospect of lower oil prices leading to cheaper fuel costs.

More insights from Schwab

Roth refresher: Simply, a Roth IRA is funded with after-tax dollars, meaning qualified withdrawals are generally tax-free in retirement. But there are specifications around eligibility and contributions. Our new retirement planning article has all the details.

" id="body_disclosure--media_disclosure--252376" >Roth refresher: Simply, a Roth IRA is funded with after-tax dollars, meaning qualified withdrawals are generally tax-free in retirement. But there are specifications around eligibility and contributions. Our new retirement planning article has all the details.

Chart of the day

Data source: Nasdaq. Chart source: thinkorswim® platform.

Past performance is no guarantee of future results.

For illustrative purposes only.

The Nasdaq Composite ($COMP—candlesticks) slipped just below previous support levels on Friday, hitting the lowest level since May 4. It was the third test of that zone of support in the past two months. The index is forming a falling wedge (white trendlines).

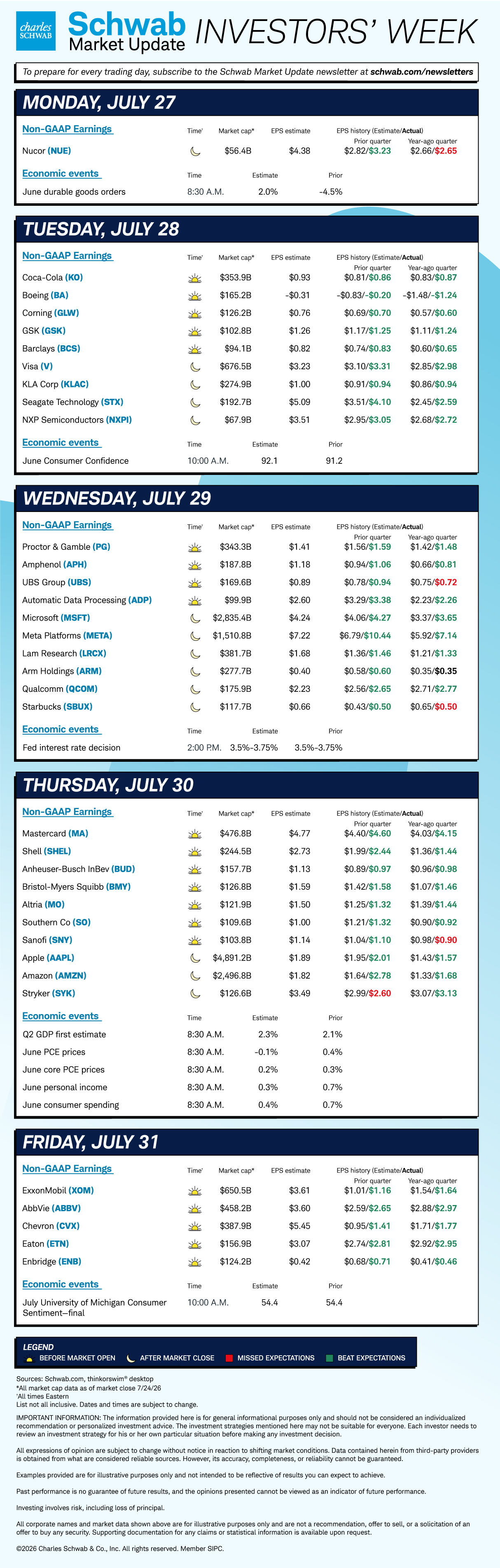

The week ahead